Create a free WunderTrading account to access automated crypto trading tools.

The Market Neutral Bot automates crypto futures spread trading by using statistical models to detect price relationships between cryptocurrency pairs. It analyzes historical market data, identifies cointegrated assets, monitors spread deviations, and opens long-short positions based on data-driven entry conditions.

No credit card required.

Automate market-neutral futures strategies to trade statistical price relationships, reduce directional exposure, and manage long-short positions with structured risk controls.

Reduce directional market exposure

Trade statistical spread opportunities

Use cointegration-based pair selection

Manage risk with automated controls

The WunderTrading Market Neutral Bot uses a statistical arbitrage approach designed for crypto futures pairs. Instead of relying on a single bullish or bearish forecast, the bot analyzes historical price relationships between cryptocurrencies and looks for temporary spread deviations.

The bot uses 3 months of historical price data, groups coins by volatility, tests pairs for cointegration, ranks potential spreads, and standardizes spread movement using Z-scores. When entry conditions are met, it can open multi-leg long-short positions and manage exits based on configured rules.

The bot uses 3 months of historical price data to group coins by volatility and prepare them for statistical spread analysis.

The bot evaluates cryptocurrency combinations and uses cointegration testing to identify pairs with a long-term statistical relationship.

Selected spreads are standardized into Z-scores, helping the bot detect when a spread moves outside its normal range.

When entry conditions are met, the bot executes multi-leg orders and can close positions when the spread normalizes or risk controls are triggered.

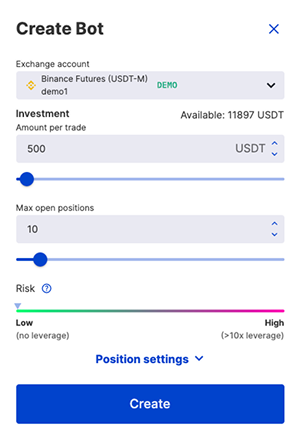

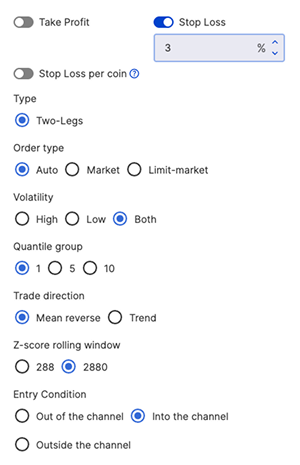

Configure risk, execution, volatility, and entry settings to control how the bot identifies and manages market-neutral futures positions.

Defines the percentage by which the spread price must move in your favor before the position is closed automatically with a profit.

Defines the percentage by which the spread price must move against your position before the bot triggers an automatic exit at a loss.

Closes the entire spread position if any single leg declines by the specified percentage.

Choose whether the bot should trade high-volatility spreads, low-volatility spreads, or both.

Set how extreme a spread deviation must be before the bot considers entry, using 1%, 5%, or 10% quantile groups.

Choose between Mean Reversion and Trend logic depending on how you want the bot to react to spread movement.

Select the rolling window used to calculate spread deviation, such as 288 or 2880 periods.

Choose whether the bot enters when the Z-score moves out of the channel, into the channel, or outside the normal range.

Traders

Bots

30-day Volume

Trade all accounts simultaneously (applies to any single exchange per trade). See the full list of supported exchanges and features by exchange for more details.